The Gaussian (Normal) distribution is a probability density function specified by two parameters – mean  and variance

and variance  . If a single variable, say

. If a single variable, say  , is normally distributed the density function is abbreviated as

, is normally distributed the density function is abbreviated as  . The square root of the variance is called the standard deviation

. The square root of the variance is called the standard deviation  . The inverse of the variance is called the precision

. The inverse of the variance is called the precision  . The function is defined as follows

. The function is defined as follows

![\begin{equation*} p(x) = \frac{1}{\sqrt{2 \pi } \sigma} \text{exp}\Bigg[\frac{1}{2} \Bigg( \frac{x - \mu}{\sigma} \Bigg)^2 \Bigg] \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-82586989505a6e87096258fd35d56078_l3.png "Rendered by QuickLaTeX.com")

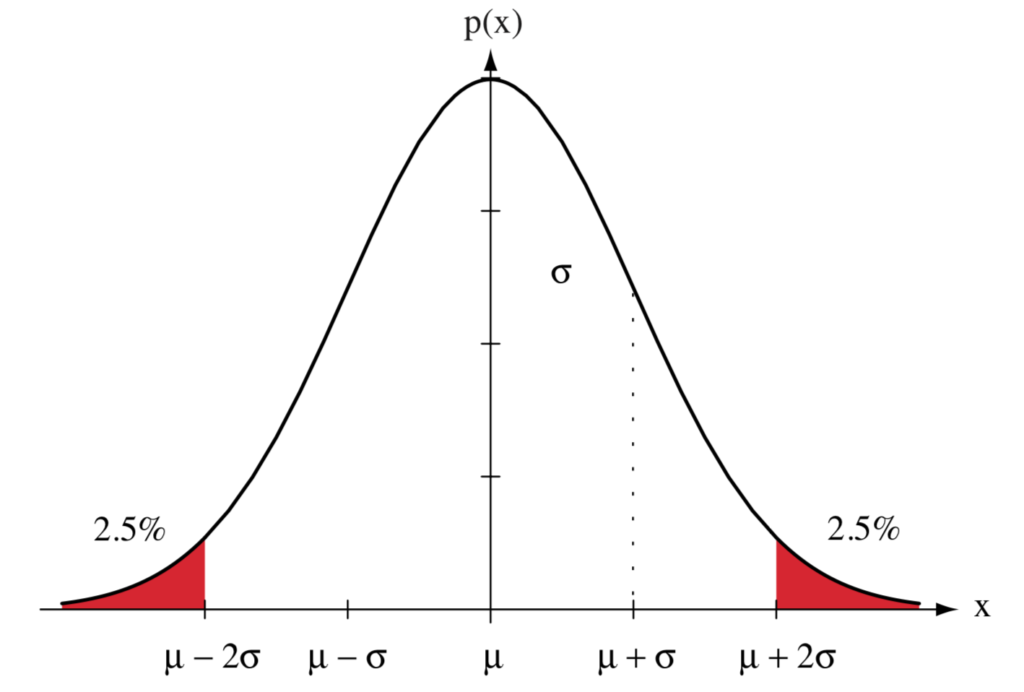

Visualization

95% of the area under the Gaussian distribution curve lies within 2 standard deviation units about the mean.

Positive

Because of the exponential term, the above density function is always positive.

Maximum

The peak of the Gaussian distribution occurs when

Normalized

Over the entire feature space, the density function integrates to 1, thus making it a valid probability distribution.

Define

Substituting and using the fact that  is an even function

is an even function

![\begin{equation*} = \int_{-\infty}^{\infty} \frac{1}{\sqrt{2 \pi } \sigma} \text{exp} \Bigg[ \frac{1}{2} \Bigg( \frac{x - \mu}{\sigma} \Bigg)^2 \Bigg] dx\end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-3d3425047dbf866e2fe1f96e99254db1_l3.png "Rendered by QuickLaTeX.com")

There are several tricks to solve this definite Gaussian integral by using the following property

Define

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \int_{0}^{\infty} \int_{0}^{\infty} e^{-(a^2 + b^2)} da \, db \Bigg]^{\frac{1}{2}} \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-a319f0272521cf9c4eb4feec7b4bdfcd_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \int_0^\infty \left( \int_0^\infty e^{-(a^2 + b^2)} \, db \right) \, da \Bigg ]^{\frac{1}{2}} \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-a1cc6c4fbb129fb6d8cb52fb4bd11abb_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \int_0^\infty \left( \int_0^\infty e^{-a^2(1+s^2)} a\,ds \right) \, da \Bigg ]^{\frac{1}{2}} \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-df7459466a42be7816dba03a62e824c3_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \int_0^\infty \left( \int_0^\infty e^{-a^2(1 + s^2)} a \, da \right) \, ds \Bigg ]^{\frac{1}{2}} \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-8ddfc86cdf0c0ca2c2e0fad8254281a1_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \int_0^\infty \left[ \frac{1}{-2(1+s^2)} e^{-a^2(1+s^2)} \right]_{a=0}^{a=\infty} \, ds \Bigg ]^{\frac{1}{2}} \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-2f1fdd1f27b937a4adca7e75532db49a_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \frac{1}{2} \int_0^\infty \frac{ds}{1+s^2} \Bigg ]^{\frac{1}{2}} \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-77f7617b1f4e50de052a71286cbc43b0_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \frac{1}{2} \Big [ \tan^{-1} s \Big ]_0^\infty \Bigg ]^{\frac{1}{2}} \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-d8d3af09e5879ea7e9a91605c23536bd_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \frac{2}{\sqrt{\pi }} \Bigg[ \frac{\pi}{4} \Bigg ]^{\frac{1}{2}} = 1 \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-407002ca893424fb3dd26c46006c9af0_l3.png "Rendered by QuickLaTeX.com")

Mean

The mean is defined by the expected value of the input variable over the entire feature space

![\begin{equation*} \mathcal{E}[x] = \int_{-\infty}^{\infty} x p(x) \, dx \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-648cb18242ac959345dbb4e2e7d51ab9_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \int_{-\infty}^{\infty} x \frac{1}{\sqrt{2 \pi } \sigma} \text{exp} \Bigg[ - \frac{1}{2} \Bigg( \frac{x - \mu}{\sigma} \Bigg)^2 \Bigg] dx \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-c837d5382e0af2870cb9c8b9b805915d_l3.png "Rendered by QuickLaTeX.com")

Define

Substituting

![\begin{equation*} \int_{-\infty}^{\infty} (a + \mu) \frac{1}{\sqrt{2 \pi } \sigma} \text{exp} \Bigg[ - \frac{1}{2} \Bigg( \frac{a}{\sigma} \Bigg)^2 \Bigg] da\end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-0c9b3b9cda2847276b0263bdb9f1102f_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \int_{-\infty}^{\infty} a \frac{1}{\sqrt{2 \pi } \sigma} \text{exp} \Bigg[ - \frac{1}{2} \Bigg( \frac{a}{\sigma} \Bigg)^2 \Bigg] da \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-2e89cb3abf62df93f5ad2b8cee8ba36d_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} + \mu \int_{-\infty}^{\infty} \frac{1}{\sqrt{2 \pi } \sigma} \text{exp} \Bigg[ - \frac{1}{2} \Bigg( \frac{a}{\sigma} \Bigg)^2 \Bigg] da \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-91dedf44e207304da029cd0af5fafa99_l3.png "Rendered by QuickLaTeX.com")

The first term integrates to 0 because the integrand is an odd function and the integral is over the entire feature space. The integrand in the second term is another (zero-mean) gaussian distribution and as such integrates to 1 over the entire feature space. Thus

![\begin{equation*}\mathcal{E}[x]=\mu\end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-5a1ab91bed9c1a1668e24b7190f182c4_l3.png "Rendered by QuickLaTeX.com")

Variance

The variance is defined by the expected squared deviation of the input variable from the mean over the entire feature space.

![\begin{equation*} \mathcal{E}[(x - \mu)^2] = \int_{-\infty}^{\infty} (x - \mu)^2 p(x) \, dx \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-b6bf5714b67a68328e14beea561214e5_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} = \int_{-\infty}^{\infty} (x - \mu)^2 \frac{1}{\sqrt{2 \pi } \sigma} \text{exp} \Bigg[ - \frac{1}{2} \Bigg( \frac{x - \mu}{\sigma} \Bigg)^2 \Bigg] dx \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-173c8c5371127ac6fa76bd32bd421025_l3.png "Rendered by QuickLaTeX.com")

Define

Substituting

Using integration by parts

![\begin{equation*} \mathcal{E}[x] = \frac{2 \sigma^2}{\sqrt{\pi}} \Bigg( \Bigg[ a \frac{-1}{2} e^{-a^2} \Bigg]_{-\infty}^{\infty} - \int_{-\infty}^{\infty} \frac{-1}{2} e^{-a^2} da \Bigg) \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-118cbc0950011e29ed90709a1998883e_l3.png "Rendered by QuickLaTeX.com")

The first term integrates to 0 because the integrand is an odd function and the integral is over the entire feature space. The second term is the Gaussian integral which evaluates to  . Thus

. Thus

![\begin{equation*} \mathcal{E}[x] = \frac{2 \sigma^2}{\sqrt{\pi}} \frac{\sqrt{\pi}}{2} = \sigma^2 \end{equation*}](http://thebeardsage.com/wp-content/ql-cache/quicklatex.com-6d5405b3e2eca4f1c6e07a9aa64e34e4_l3.png "Rendered by QuickLaTeX.com")